7 Ways to Prove Marketing ROI to Your Clients

See also: Strategic MarketingHow do you convince a client that their marketing campaign running to hundreds or thousands of dollars is yielding results without sounding silly?

It’s hard enough to explain tangible marketing return on investment (ROI), but what about the intangible ones without immediate results?

Yup. It’s for reasons like these that 23 percent of marketers struggle to meet client expectations.

The way out is simple — prove marketing ROI, or balk under client pressure.

Your ability to prove evidence-based ROI to clients will influence future marketing projects and the client’s willingness to increase their marketing budget.

Read on to learn seven ways to prove marketing campaign return on investment to your clients.

1. Set Your Key Performance Indicators

KPIs are the performance metrics and indicators you need to track to ensure you’re in profit or hitting campaign-specific goals.

Your client may have an idea of what progress looks like — but some of these expectations might be unrealistic from a marketing perspective. Discuss with your client to set these abstract KPIs straight and understand their overall expectations. Then, come up with the best possible strategy to hit the goals.

Your KPIs must be quantifiable and measurable. Though, it’s usual for each campaign to have its own KPI. For instance, if a campaign’s objective is to “increase company-wide revenue by 50 percent” then revenue growth KPIs like sales growth rate, net profit margin, or financial spend per department may serve as metrics.

On the other hand, a “grow website traffic by 30 percent yearly” campaign will require you to track KPIs like acquisition metrics, number of site visitors, average time spent on the website, etc.

Thus, you should be clear from the start on what KPIs and metrics to use over a period of time. Standard metrics to track when demonstrating marketing ROI are:

- Clicks

- Advert engagements

- Conversions

- Lead generation

- Cost per acquisition

- Cost per lead

- Revenue growth

- Customer lifetime value (CLV)

While you can measure some metrics with built-in analytics on social platforms or email software, you can also use third-party web applications like Cyfe and Google Analytics to forecast a projected ROI.

2. Forecast Expected Returns

Forecasting marketing ROI is difficult but necessary. See it as a realistic path to success based on your experience and available data.

Marketing return projections help you determine the profitability of a marketing campaign ahead of time without giving clients unrealistic expectations.

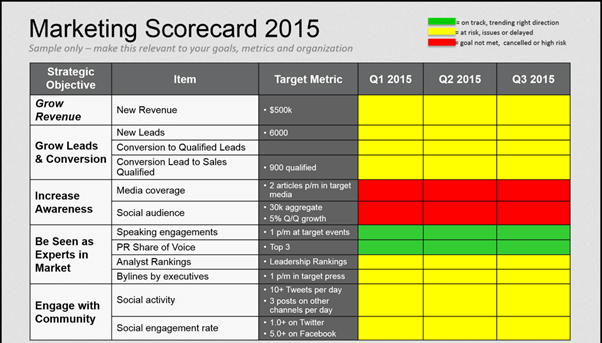

Since it’s easy to get overwhelmed with all that marketing data, the easiest way to forecast expected returns is with a scorecard.

Marketing scorecards compare the potential or actual return on investment for all channels in one spreadsheet, making it easy to:

- Compare campaign data across channels

- Project marketing ROI, and

- Spot weak links in your marketing plan, such as poor CTR.

What you need to do is fill in the necessary data relevant to your campaigns, such as channel, conversions, spend, CPC, and other conversion metrics, in the scorecard template.

Using vendors' estimates and historical data from your analytics, you can determine the expected return for each channel and source you evaluate. That gives you a rough idea of the campaign’s profitability and the relative efficiency of each investment. These projections become the campaign goals during the launch.

As actual data becomes available, you can replace your estimates with them to see real returns on investment.

Scorecards also allow you to analyze performance against goals. Calculate the variance, and then use that information to modify mid-campaign metrics or increase forecast accuracy. For example, you can opt for automation when sending recurring emails, doing follow-ups, or performing other functions like outreach to optimize the ROI.

3. Estimate Marketing Costs of Your Clients

Estimated marketing costs are your client’s would-be marketing expenditures for a campaign.

These costs include marketing expenses needed to make a campaign successful. It can be paid ad credits and marketing spend for content marketing and email marketing, website design, and software subscriptions.

To develop a marketing budget:

-

Identify specific short and long-term marketing goals as part of a bigger marketing plan.

Understand market trends to cater to exterior forces that may impact and affect the return on marketing investment.

Research and learn from the competition so you can understand their ads and marketing strategies to optimize them for your own campaign.

Choose the best marketing channels for improved ROI.

Estimated marketing costs are dependent on campaign type and marketing channel. Monitoring each cost per channel will help you distribute your marketing budget efficiently and optimize each channel for the best results.

You can also calculate estimated marketing costs to see which impacts ROI the most. That will help you make informed decisions concerning marketing expenditures and justify every expense.

Eventually, you’d be able to instigate better customer relationships as your clients begin to trust your expertise and rely on your ability to estimate these costs.

4. Determine Customer Lifetime Value (CLV)

Customer lifetime value describes how a business benefits from interactions with customers over time. It's also a significant way to help your clients calculate marketing returns.

Sometimes your client might not consider CLV a necessary metric to track because the benefits aren’t immediate. However, it’s your job to sell the benefits of a returning customer and, possibly, tweak your campaign to recall old customers.

You can win back customers with personalized drip campaigns or via retargeting ads, for example. Once you begin to see results from your campaign, include the CLV in your calculations.

A simple formula to calculate CLV is to multiply the annual revenue of a customer by the average lifetime of that customer minus the initial acquisition cost.

Customer Lifetime Value = [Annual Revenue per Customer x Customer Relationship in Years] - Customer Acquisition Cost

This basic formula makes it easy to justify your client’s marketing budget. But you can only use this if annual customer revenue is flat such as in a one or two-tier SaaS subscription-based model.

However, when the annual customer revenue isn’t flat, you should calculate the customer retention rate instead.

Gross margin x [Retention rate / [1 + Rate of discount - Retention rate]]

The formula considers discount rates and fluctuations in customer revenue over time. You can also adjust the discount rate to accommodate inflations for accuracy.

While CLV can help you make projections and regulate marketing budget distribution, tracking each customer’s CLV is tricky and varies. Ensure you’re clear on the CLV metrics to track from the onset and prove how it impacts the client’s business.

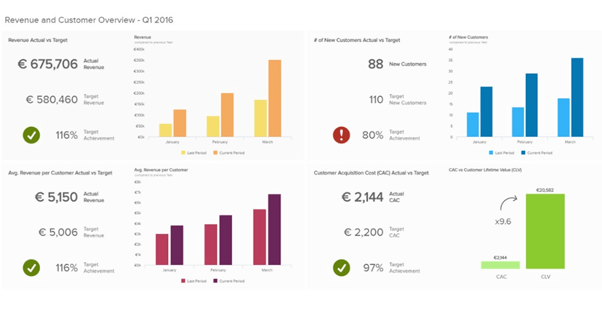

5. Build An Effective Dashboard

Marketing data can be overwhelming, so build an effective dashboard to simplify your data visually.

Now, decide on the most valuable data to showcase and design your dashboard in an easily understandable way. Leveraging a data analytics platform like Zoho or Datapine will do you much good and provide real-time data for clients.

An effective dashboard should show clients concise reports on online and offline campaign performance and a cohesive view of all ROI measurements integral to the business.

6. Calculate Returns from Each Campaign

To prove marketing returns, start by analyzing the strategies used in simple campaigns like content marketing, email marketing, or social media marketing to know the ROI value of each campaign.

That helps to identify well-performing campaigns and pitch them again for future use.

CRM software and Google Analytics can gauge the success of your campaigns and show you where to make adjustments to improve profitability.

7. Provide Relevant Recommendations

Businesses hire marketing specialists like you for their expertise. They believe you have what it takes to boost business growth and will take your word for it. For this reason, when presenting marketing ROI to clients, be confident and make relevant recommendations based on available data.

You can do this through emails or by setting up a video meeting. Then adapt your strategy based on conclusions reached with your client. After all, your clients are only concerned about one thing at the end of the day — marketing returns on investment.

Providing relevant recommendations would build more trust and increase your chances of a higher budget in the future.

Final Thoughts

Your marketing agency is responsible for providing the highest returns on marketing investments and showing proof that your client’s money was well spent. But your results must speak for you.

Put realistic KPIs in place and establish a benchmark for ROI expectations. Estimate marketing costs based on spending priorities so you don’t micromanage and come up short mid-campaign.

As you proceed with each campaign, make relevant suggestions and project expected returns to explain possible ROIs without immediate results. Be clear on expectations and don’t over-promise on any campaign — you might balk under pressure.

Provide value to your clients with these tips in your next campaign!

About the Author

David Campbell is a digital marketing specialist at Ramp Ventures and helps manage the content marketing team at Right Inbox. When he's not working, he enjoys traveling and trying to learn Spanish.